Today I got asked, by a couple that has very good financial hygiene, whether it’s okay for them to forego saving over the next three years. Between their kids’ education, a career change, and some wanted home renovation projects, there just isn’t enough money to save on top of it all. Is this an okay financial decision?

To answer the question, let’s look at some curves:

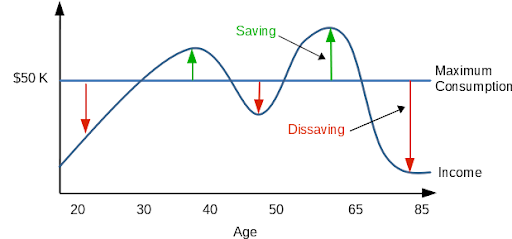

THE FINANCIAL LIFE CYCLE CURVE

What the above graphic illustrates about saving vs. spending is that nobody realistically can or will, save in every year of their life. For most people, their wealth accumulation years are between ages 30 and 65. Their non-accumulation years are between ages 1 and 29, and their deacumulation years are ages 65+. Moreover, someone in their wealth accumulation years won’t save every year for many possible reasons such as a career change, loss of job, home renovations, or college tuition expenses. This means that more than 60% of the time, one can not be reasonably expected to save, and that’s okay.

A very important distinction though is that just because a person isn’t saving, doesn’t mean that their net worth will decline. A $1,000,000 portfolio can easily pay out $25,000 and still potentially increase in total value over the course of a year. The flip side of all of this is, of course, if a person only has approximately 30 years when they realistically can be expected to save, then it is very important to make hay while the sun shines. That is all to say, save lots of money in your good earnings years!

What do Wealth Accumulators need to be thinking about?

-

- Designing your life so that you can save – Notice that I didn’t use the word “budget” here. To many, budgeting implies going through your expenses line by line and eliminating the “unnecessary,” but the reality is that so much of spending is built-in that the budgeting exercise often falls flat. A much more effective approach, albeit longer-term, is around lifestyle design: get a job that pays you well, drive an economical car, choose a house and neighborhood to live in that won’t blow up your monthly expenses. The goal is for your monthly income to be sustainably higher than your expenses.

-

- Investing for growth – If you’re in your 30s or 40s, time is on your side. Stocks have historically outperformed bonds over longer time periods so as a young investor, you get to patiently wait out periods of stock market volatility while compound growth does its job over the long-term.

-

- Managing your future tax liability – 401(k)s are unabashedly wonderful if you get a match, however the benefits of deferring income taxes and not paying capital gains have a downside. We often see 401(k) millionaires who don’t realize they have a huge outstanding tax liability when they start withdrawing in retirement. Further, having money locked into retirement accounts can be a problem when it comes time to pay college tuition or buy a second home. There’s no one-size-fits-all answer here, but finding the right balance between retirement accounts and taxable brokerage accounts is key.

What do Wealth Deaccumulators need to be thinking about?

-

- Not running out of money – Again, the key is lifestyle design, not budgeting. Work part time in retirement? One home or two? How much to travel? Give money away? Live on IRAs before starting Social Security? Frankly, it’s imperative to get these decisions right because you can’t fix overspending mistakes with your wages like you used to.

-

- Portfolio construction – While younger investors might find success “setting it and forgetting it” in Vanguard index funds, a retiree’s portfolio will need much more careful construction around timing of distributions, bond laddering, and volatility management. How much money to take out, when and from which account to withdraw it are very important questions.

-

- Tax liability of distributions – How do you get your money out of your 401(k) without triggering too much taxable income? The answer is often a few well-timed Roth Conversions to get your tax-deferred assets out when it’s the most advantageous, combined with delaying Social Security.

Saving, aka Wealth Accumulation, isn’t mandatory in every year of our lives and it is actually very okay to intentionally not save in the majority of the years of our life. What’s most important is saving lots when it is possible and, when it is not possible (retirement), to be intentional about it and to avoid costly pitfalls.