{I recently had the opportunity to meet with some people in their late teens to answer their questions. This is the letter I wrote them afterward.}

The thing with being an adult is that you generally have to hear the same information from a couple of different directions before it starts to gel. So the stuff I talked with you about last night is once, and this email can be a second, and then when you encounter these concepts later in the wild you’ll be ready for them to click.

We talked about a number of different topics. I’m going to break them out that way in this email so you can skip to the part you are ready to listen to. 😉

Regarding taxes, here are three things you should know:

I told you that the Federal withholding tables are broken. You probably shrugged and figured it was some sort of political commentary or something: surely the government couldn’t do something so basic so very wrong? But the Federal withholding tables only really work if you’re a one-job household. One job just doesn’t know what the other job will make. So the solution here is to aim to make sure your withholding is around 10% for the Federal taxes once your income is over about $12,000/year. You can change the W-4 anytime you want. I generally recommend putting 0 for the exemptions and then adding extra to be withheld each week once you’ve looked at a paystub and can see how the withholding will work. (The state withholding tables work, just say 0 exemptions and you’ll be fine.)

Tax returns are a reconciliation tool to put down what you REALLY earned and what you REALLY paid in taxes already, then compare it to what is calculated you’d owe now that the whole picture is in place. The tricky part isn’t usually figuring the tax, it’s figuring the taxable income after we throw in the things that you are allowed to deduct against it.

We also use the tax return to administer a bunch of anti-poverty programs like the Earned Income Tax Credit, and to disperse tax credits for things like tuition paid and solar panels installed, things like that. It’s just a handy moment to total up what the government owes you as they’re generally based on your income.

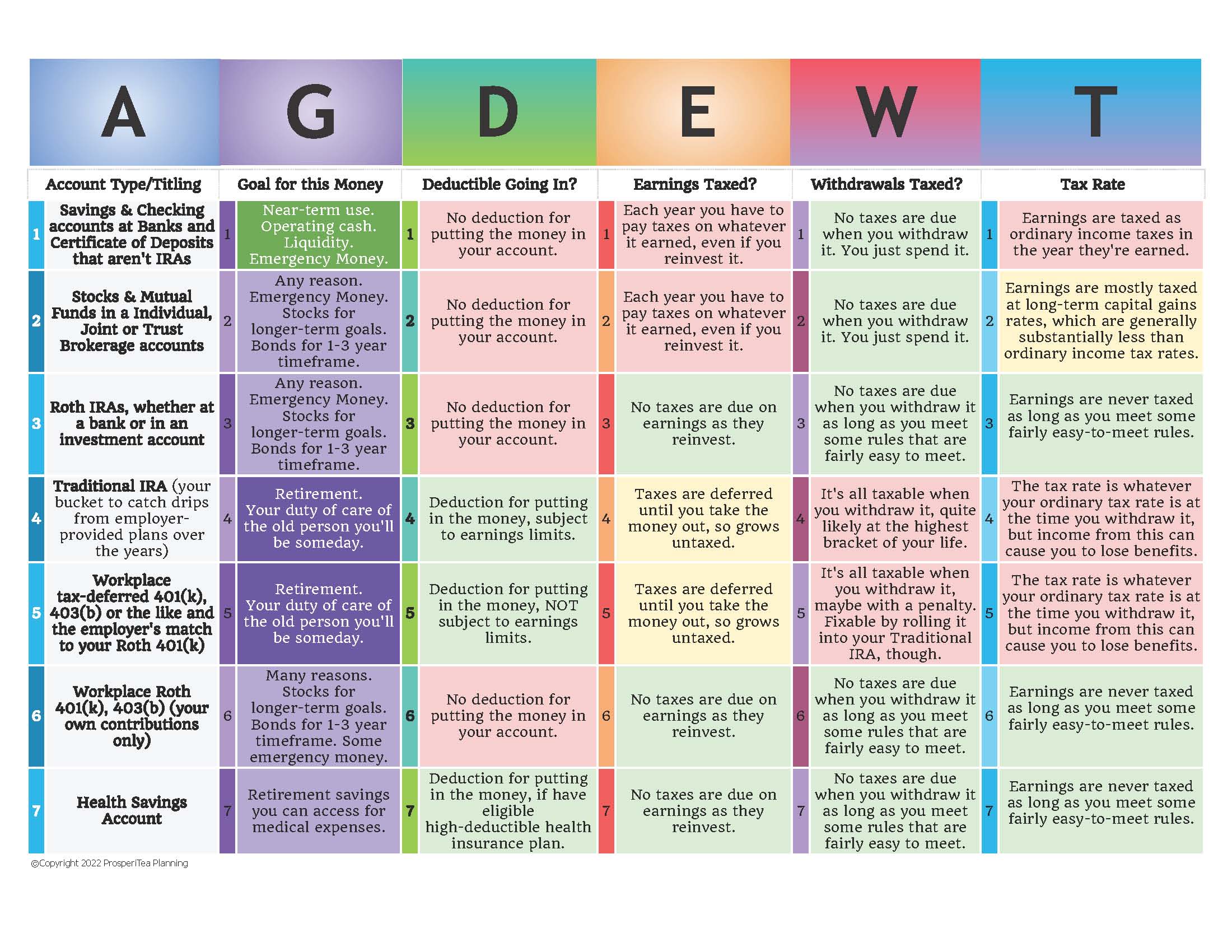

I spent WAY too much time making this chart beautiful!

Types of accounts. We talked about how you can “title” an account in a bunch of ways, which will cause them to be taxed differently.

The basic default type of account is to title it as an individual or joint checking at a bank, or an online savings account (individual or joint). But there are several other types of accounts. This is beautifully illustrated (if I do say so myself) in the AGDEWT chart on the left. Click to embiggen. But the short version is that besides bank accounts, there are also:

- Individual or joint brokerage accounts,

- Roth IRAs (IRAs stand for Individual Retirement Arrangement: they can’t be joint.)

- Workplace tax-deferred and Roth accounts,

- Your own Traditional IRA (that I referred to as a bucket to collect all the drips from previous employer plans, and

- Health Savings Accounts are for people who ever had a high-deductible health insurance plan.

How to do a budget/bill-pay.

I mentioned that Quicken is a great checkbook register program that you can use to track all your past spending, but it’s not very helpful for figuring out where your next dollar should go. For that, the killer app is YNAB.com, a program that lets you tell your money where it needs to go to fill up envelopes for essential spending (groceries, rent) but also rainy day spending (new tires, winter clothes). It’s good in conjunction with short-term savings accounts like at Ally.com, but also really helpful for building up a rainy day cushion in your operating bank account. Two of my adult children use it, while the third uses his self-made excel sheets. The gist of it is to make sure money is where it needs to be when it needs to be there. Otherwise, you’ll see money accumulating and think, “oh, I’ve got money for a weekend in Vermont!” when you ACTUALLY have money saved towards the expected vet bills an old cat will have.

We also talked about how emergency money is DIFFERENT than rainy day money. Emergencies are for things you don’t expect. If nothing unexpected happens, it’s for old age. On the other hand, it rains every other day. Rainy day money is a way to spread out likely annual expenses that WILL land, we just don’t know when exactly.

We talked a bit about how it’s nice to have parents that help you with large capital expenses that provide you with a start in life, but how it’s somewhat infantilizing for them to help you with everyday operating costs. The need to buy groceries and pay your car insurance bill is what forces you to do the annoying work of getting a job.

I talked about the best way to fix a budget: earn more. A great book that made a big impact on me years ago was Overcoming Underearning by Barbara Stanny. Another trick is to ask a man what he’d accept as a salary and then ask for that! (Women tend to accept 15% less than men, uggh.)

A great idea is to do a moonlighting job to save for a short-term goal (like replenishing your emergency money). We learn in ALL our scut jobs. Don’t look down on any.

I talked about “massive action”, and visualizing your best life.

I asked you to stop and do some dreaming about what your perfect life will be like when you’re 28. Where are you? City or country? Are you working with people or alone? Are you working inside or outside? Are you doing detailed work or is showing up and doing your best each day enough to succeed? (Accountants can’t say “meh, close enough”, but teachers sort of can!) Do you want to be sitting at a desk or moving around during the day? Do you want the safety of a career in a governmental agency, or would you like the risk/reward of being self-employed? Just sit and imagine your best possible life. Don’t worry about trying to figure out how to get there, just really VISUALIZE what success would look like to you. This exercise is super useful because you’ll now be primed to notice an opportunity as it arises that might lead you in that direction.

Massive action is where you commit to taking action until you get your desired result. If you apply for 3 jobs you might not get one. But if you keep applying, using what you’ve learned, after 300 you certainly will!

We talked about going to grad school in a non-funded program straight out of college. That’s usually a terrible idea. A far better idea is to go work for a while in the general industry you’re thinking of joining after grad school and see what you like. Even better is to try to get a job at a place that pays tuition for its employees. I’m paying for my paraplanner to become a Certified Financial Planner. Colleges give tuition waivers to their employees. Various agencies will pay for you to get a graduate degree in the field they’ve hired you into. Look for those jobs.

I have more to say about retirement plans, but that’s a story for another day.

Wendy Marsden, CPA CFP®

January 1, 2023